2 months ago

10

2 months ago

10

Wall Street has been debating the SaaSPocalypse for months, if not years. Goldman Sachs studied how hedge funds and mutual funds are approaching the space—and found a major shift in investing.

Software & Services as an industry group is down 14% year-to-date and has lost 9% over the last 12 months. Semiconductors & Semi Equipment are up 38% YTD and have surged 104% in the past year. The performance gap is staggering, but it’s a symptom, not the cause. The cause is a fundamental reassessment of where AI value actually accrues — and the answer, increasingly, is not in the application layer.

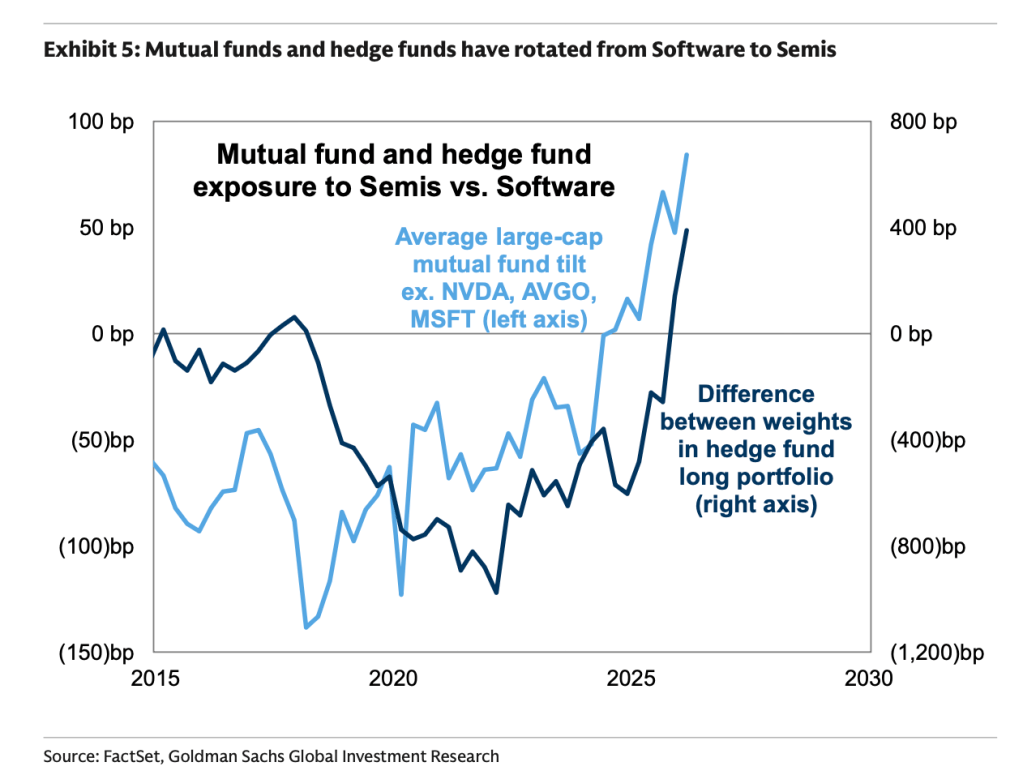

Goldman’s U.S. Weekly Kickstart, published May 22 and drawing on $9 trillion in equity positions at the start of the second quarter of 2026, doesn’t editorialize. The numbers make the case: hedge funds have cut software to its lowest weight in their long portfolios since 2019. Mutual funds are carrying their widest underweight in software (excluding Microsoft) since 2012. Both fund types, Goldman notes, “continued their recent portfolio rotations away from Software and toward Semis” — a line buried in the middle of the report that deserves a banner headline.

This is not panic. Hedge fund net leverage is running at the 85th percentile of the last five years. These funds are not de-risking. They are making a deliberate, consensus call — in broad daylight, with near-record overall exposure — that software is the wrong place to be.

Hedge funds added to LRCX, AMAT, and ASML on net during Q2. Mutual funds piled into INTC and SITM. Even Microsoft — the one software company that was supposed to be AI-proof, the one name that always survived the rotation — was cut on net by both hedge funds and mutual funds last quarter.

Goldman’s own earnings projections capture the skepticism baked into its strategists’ models. Info Tech is forecast to grow earnings by 31% in 2026 — but Goldman’s top-down estimate of $92 in sector EPS contribution runs well below the $106 projected by the bottom-up analyst consensus. Fortune reported in November that Goldman’s top analysts had flagged U.S. tech stocks as likely to underperform over the next decade — a call that looked contrarian then and looks prescient now.

What “recovery” actually means now

Here is the cold-water version of the bull case: software doesn’t die. As Fortune examined in March, Wall Street’s conviction that AI will kill SaaS runs up against a stubborn historical pattern — platform shifts tend to enrich incumbents who adapt, not destroy them. Economists and technology historians cited in that piece argued that existing vendors with deep customer relationships and proprietary data are better positioned than newcomers to capture the upside of agentic AI. JPMorgan analysts have made the same case, pointing to long-term contracts and switching costs as structural moats that won’t evaporate overnight.

Goldman has separately projected that the global app software market is still projected to hit $780 billion by 2030, and that agentic AI would expand the overall software pie significantly by the end of the decade. JPMorgan analysts have pointed to long-term contracts and switching costs as structural moats that won’t evaporate overnight.

But none of those arguments say the era of 20x revenue multiples will return, or that seat-based subscriptions will reprice upward. The bull case for software in 2026 is that the incumbents survive the transition well enough to bolt on new capabilities, reprice around usage rather than seats and hold on to their data advantages long enough to matter.

The enterprise is already sending the same signal from the demand side. Fortune reported in April that CIOs and CTOs have begun taking a significantly harder line with their software vendors — renegotiating contracts, demanding outcome-based pricing, and openly threatening to replace tools that can’t demonstrate AI-native capabilities.

Thomson Reuters CTO Joel Hron put the sharpest point on it in a Fortune commentary last week: the real dividing line isn’t SaaS versus AI agents. It’s companies with deep, proprietary, domain-specific data — the kind that can train and differentiate an AI model — versus companies that are essentially interface wrappers.

It’s a distinction that ServiceNow, for one, has clearly internalized. At its Knowledge 2026 conference earlier this month, executives didn’t bother defending the SaaS model — they declared it over. “The era of sidecar AI is over,” president and COO Amit Zavery told Fortune from the conference floor. “Customers don’t want to cobble pieces together — they want outcomes.” What ServiceNow is betting on instead is its Context Engine: a governance layer built on 100 billion workflows and 7 trillion annual transactions that it argues gives AI agents the contextual guardrails to function reliably inside a real business. “Enterprise software was never sexy,” Zavery said. “The amount of time people building software in this space spend — not just building features, but making it secured, compliant, guaranteed performance … all those things are never sexy jobs. They’re very heavy, painful, getting into the nitty-gritty, making sure you’re solving the difficult problems.”

The Goldman self-contradiction is worth watching

The most provocative thread in this story may be Goldman’s own. In March, the firm published research finding no meaningful relationship between AI adoption and productivity — except in two specific areas: customer support and software development. Those are the exact workflows that SaaS platforms were built to manage. The implication cuts both ways — AI is genuinely disrupting the use cases software was designed to own, but the productivity gains are real and measurable, which means someone is capturing them. The question is who.

Then in May, Fortune reported on Goldman research finding that FOMO — not rational capital allocation — is a key driver of the AI infrastructure boom, with the firm quietly concluding that hyperscalers are “prioritizing being involved in the AI arms race over their current shareholders.” If the semis supercycle is itself running partly on narrative, then the rotation eating software’s lunch may eventually face its own reckoning.

That complication doesn’t save software. But it does suggest the story isn’t as clean as the positioning data makes it look.

For this story, Fortune journalists used generative AI as a research tool. An editor verified the accuracy of the information before publishing.

This story was originally featured on Fortune.com